Bank of Japan Stays the Course on Negative Interest Rates

Contact

Bank of Japan Stays the Course on Negative Interest Rates

Even if fiscal policy requires further expansion due to the pandemic.

-

Credit: Asian Development Bank licensed under CC BY.

Credit: Asian Development Bank licensed under CC BY.

Haruhiko Kuroda, Governor of the Bank of Japan (BOJ), said September 8th that the central bank will continue to keep interest rates low even if that requires further expanding fiscal policy according to an interview with Nikkei Asia.

With this signal, Kuroda is differing from his European and American central bank counterparts who are currently looking for ways to reduce their own monetary easing.

This means that interest rates on property loans are not likely to rise anytime soon despite the pandemic. Currently owner occupied home loans on a max 35 year loan term are going for sub 1 percent interest.

For buy-to-let property lending, rates are relatively low at sub 2 percent for up to 30 years however, according to real estate agent sources, banks have been rejecting loan applications even from over qualified borrowers since the beginning of the pandemic.

Most agents say the same thing; while the bank never specifically says why they reject applications, off the record bank sources cite the pandemic’s negative influence on the employment stability of lower budget renters - tenants who rent the same type of units eyed by individual property investors. If the units are empty, owners have a more difficult time paying off mortgages.

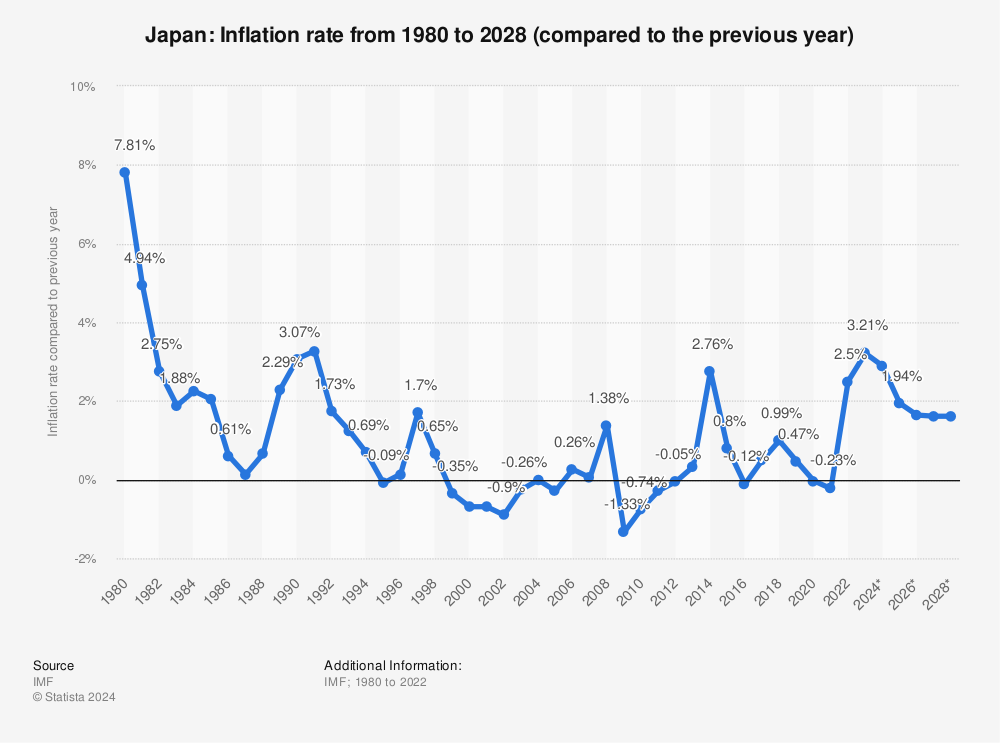

Japan's inflation rate is seen as the bellweather for when the BOJ might raise rates. Similar to European peers, the BOJ is targetting 2% annual inflation and once Japan hits this target consistently, only then will the BOJ consider easing the policy, no matter what.

While overall inflation has risen since the advent of the policy, the 2 percent target remains elusive.

Background

The BOJ announced negative interest rates in January of 2016 as a way to encourage banks to deploy capital into the economy in the form of increased lending; lending which theoretically could be used to embolden risk averse corporate Japan to try new things with less financial fear of failure thanks to very low borrowing costs.

For the BOJ, the overly conservative lending practices of Japan’s risk averse and archaic banking sector is one of the reasons for the country’s stagflation since the burst of the bubble in the early nineties.

The innovative successes that rise to the forefront due to companies being able to access cheaper loans should allow for overall employee wage increases to exceed the 2 percent inflation target, setting off a virtuous economic cycle to fuel further growth.

Video courtesy of CNBC YouTube

According to the University of Waterloo Economics Society, “The implications of negative interest rates mean depositors must pay money to set aside reserves, which is a reversal of the common understanding of economics. [Central bank] Depositors are commonly known as [retail and investment] banks, and their relationship with the Central Banks are similar to regular people who keep accounts at a local bank. This relationship normally allows depositors to receive a small amount of interest in return for leaving their money with the Central Bank.

“However, with the introduction of negative rates, Central Banks charge depositors a negative rate on principal kept in excess reserves. This strategy is meant to encourage the productive utility of money for depositors by lending more frequently to consumers and businesses. Negative rates are then supposed to send a ripple effect through the economy by lowering the cost of borrowing for everyone – which should in turn stimulate economic growth.”

Further Reading:

BOJ paying banks to boost pandemic relief, compensates for negative interest rates (Reuters; August, 2020)

Why Negative Interest Rates Are Still Not Working in Japan (Investopedia; December, 2020)

Why is Japan's monetary policy so unpopular with banks? (Reuters; September, 2018)

Most popular

Latest from our contributors